As we close out this year and look ahead to 2023, multiple questions may arise. As citizens, as workers, and as family members, we want to know: will we have a recession, and what will that mean for my loved ones and me? As investors, we watch the markets after a difficult 2022 and want to know: will we see a rebound or more declines? Overall, with everything that is happening, we wonder whether we might get something even worse, like a repeat of the Great Financial Crisis of 2008. Worry levels are high, and that is coloring everyone’s perception of the year ahead.

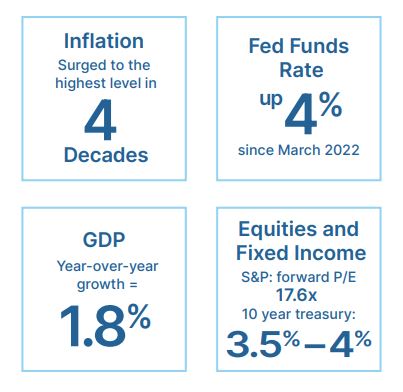

In some ways, this concern is warranted. Looking back at 2022, we have seen China struggle with the economic impact of the Covid-19 pandemic. We have seen crypto companies in the U.S. implode. We have seen the Russia-Ukraine war continue. And, of course, we have seen inflation reach 40-year highs as both stocks and bonds moved into bear markets. We know the risks are real.

When we look at the fundamentals for both the economy and the markets, however, things aren’t nearly as bad as headlines suggest. While we do face risks, the fundamentals are much stronger now than they were at the start of 2022. That should limit the risks and provide more opportunities in 2023.

The Economy

Headlines about the economy mostly revolve around inflation and the Federal Reserve (Fed), which continues to raise interest rates as we end the year. As a result of both of these factors, we can expect substantial economic slowing. Indeed, this is already apparent, especially in housing. Because the economic effects of interest rate hikes can take a year or more to show up in the economy, a recession is very possible next year if the impacts become severe enough. If we do get a recession in 2023, the good news is it’s likely to be mild and short-lived.

The reason is simple. When we talk about the economy, we are mostly discussing consumer spending, which accounts for more than two-thirds of U.S. economic activity. Consumer spending depends on the job market—you can’t spend if you don’t have income. And, generally speaking, you don’t get a severe recession without a pullback in both the job market and consumer confidence.

The good news is that both remain strong. Job growth over the past 12 months is more than twice the level typical of past expansions. There are more than 10 million open jobs. Although the labor market does seem to be slowing, it has quite a way to go before it hits recessionary levels. With such a cushion, we are unlikely to see a recession until the second half of next year, and even that isn’t a certainty. Confidence has also pulled back but remains historically high. People are making money and spending money, and that will provide support for the economy, even in the face of higher rates.

Consumers aren’t the only indicator that a potential recession should be mild. Business confidence and investment remain healthy, driven by consumer spending and the strong labor market. So, while we do see slowing and may see a recession, economic fundamentals remain surprisingly strong.

The Effects of Inflation and Interest Rates

If the economy continues to grow, however, those strong fundamentals could keep inflation higher and keep the Fed hiking, leading to a worse recession. Even though this is a possibility, it’s not what the data is indicating. Inflation appears to have peaked, with most of the components turning down, and that trend is likely to continue. While the Fed will probably keep hiking interest rates, the rate of increase—and the ultimate peak—will roll over even as inflation does. As 2022 ends, we see evidence of that in the inflation data, and also in the bond market, with the yield on the U.S. Treasury 10-year note peaking and rolling over. This likely reflects an impending slowdown but also indicates that interest rate damage may be peaking as well. All of that provides a good foundation for markets.

The Markets

Much of the market damage in 2022 was caused by higher interest rates. If rates peak, the damage will subside; if they start to decline, we could see a tailwind. The declines in bond values in 2022 were linked directly to higher rates, but as rates moderate, those declines are unlikely to repeat. Beyond that, for the first time in years, bondholders are now being paid competitive rates of interest. Although the bond market took a big hit last year, 2023 is likely to be substantially better.

For stocks, the picture is more complex but relatively positive. Stocks were also hit by rising interest rates as valuations (which depend on rates) dropped. That said, while we entered 2022 with valuations at very high levels, we enter 2023 with much more reasonable valuations. They’re not cheap, but they are in line with historical averages. From a valuation standpoint, the risk to stocks will be much lower next year.

With valuations reasonable, though, the results for stocks will depend largely on corporate earnings. Here again, the headlines are discouraging: analysts have downgraded expectations. Beyond the lower sales a recession would generate, there are also concerns about corporate margins, with higher wages and debt service costs likely to affect the bottom line. Even if valuations hold, lower earnings are a headwind for stocks.

But here, too, there is good news. While the challenges are real, both wage growth and interest rates appear to be peaking, so the damage may be less than expected. Analyst expectations typically are too pessimistic, so this would be in line with historical results. And, as previously noted, any recession will likely be mild. There is certainly downside risk, but relative to expectations, there is more upside opportunity.

The Overall Outlook

As we head into 2023, worries about the economy and the markets have largely been incorporated in expectations and prices. This means that if things are better than expected—which seems probable on multiple fronts—the results should be positive, too.

After a difficult 2022, when the economy and markets adjusted to higher inflation and interest rates, supply shortages, and multiple other shocks, the natural expectation is that things will remain bad. What we are seeing in the data, however, is that the economy is doing better than expected, and inflation is in the process of being contained. We are making progress, and that progress should continue into 2023.

Will next year be a great year for the economy and markets? Probably not. Will it be better than 2022? That’s very likely, and it could quite possibly be substantially better. As a motto, “better than it looks” isn’t ideal, but as we enter the new year, we could be doing a lot worse. So, we’ll take it.

Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Investments are subject to risk, including the loss of principal. Past performance is no guarantee of future results. This material is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product.

Authored by Brad McMillan, CFA®, CAIA, MAI, managing principal, chief investment officer, at Commonwealth Financial Network®.

© 2023 Commonwealth Financial Network®